Summarize and analyze this article with:

Note: The Ai Group’s 2026 Industry Outlook Report Signals a Workforce Rethink. The following article is IMS People Possible’s interpretation of it.

Every year, the Australian Industry Group surveys senior business leaders across manufacturing, construction, professional services, transport, utilities, and more. The2026 edition — the 13th annual survey — drew responses from 225 leaders whose businesses collectively employ over 58,000 people and generate more than $41 billion in annual revenue. Together, those sectors account for 42.6% of Australian industry value-add.

The headline finding for 2026 is blunt: one issue dominating the thinking of Australian industry leaders is managing the rising cost of doing business amid subdued economic conditions.

While that sounds like a macro problem, we think it’s a workforce strategy problem in disguise.

The Cost Squeeze Is Structural, Not Cyclical

Most commentary on the 2026 outlook focuses on inflation figures and interest rates.

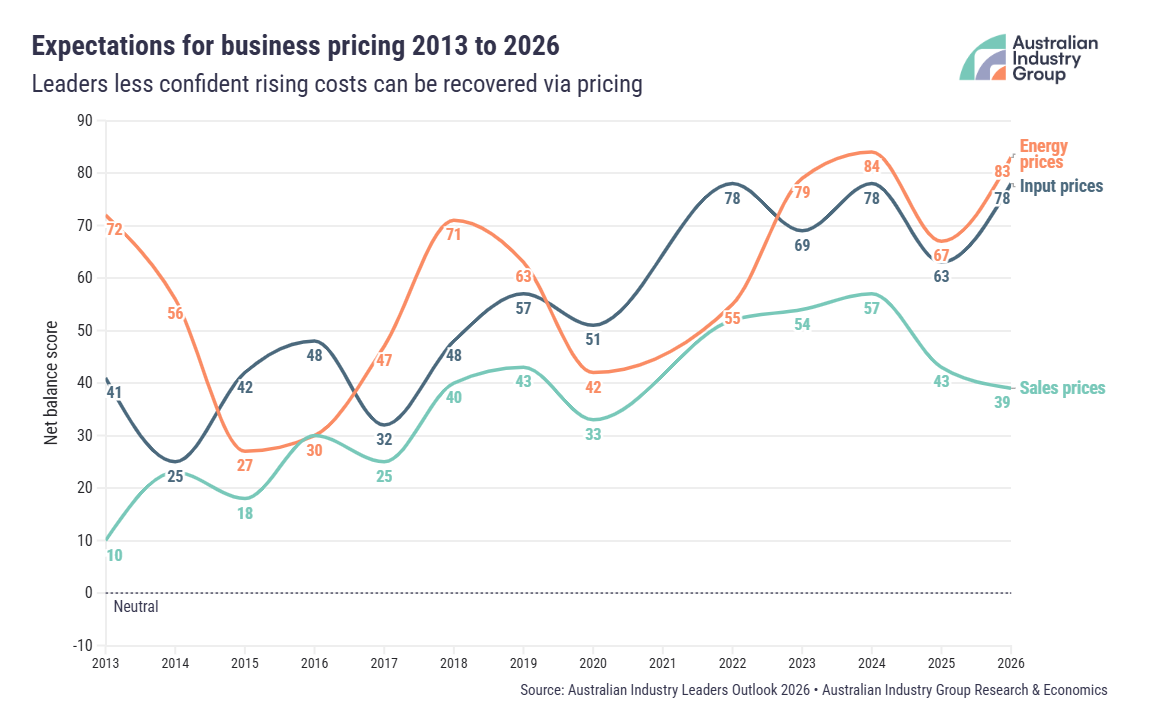

Input price expectations have hit their highest recorded level in the survey’s entire 13-year history — equal to the surge seen immediately after the pandemic. Energy price expectations have returned to 2022 levels.

But here’s the part that deserves more attention: the number of businesses expecting input and energy cost rises is double those expecting to raise their sales prices. That gap — 39 percentage points — is the largest ever recorded in the survey’s history.

That means most of the cost pressure lands directly on the balance sheet. You can’t pass it on. You have to absorb it.

Expectations for gross profit margins remain mildly negative (-2 net balance), and given the positive score for revenue growth expectations, this points to one conclusion: cost increases are likely to consume most of any revenue uplifts achieved in 2026.

Revenue up, margins flat or declining. That’s not a recovery — that’s running to stand still.

Payroll Tax Is Actively Punishing Hiring Decisions

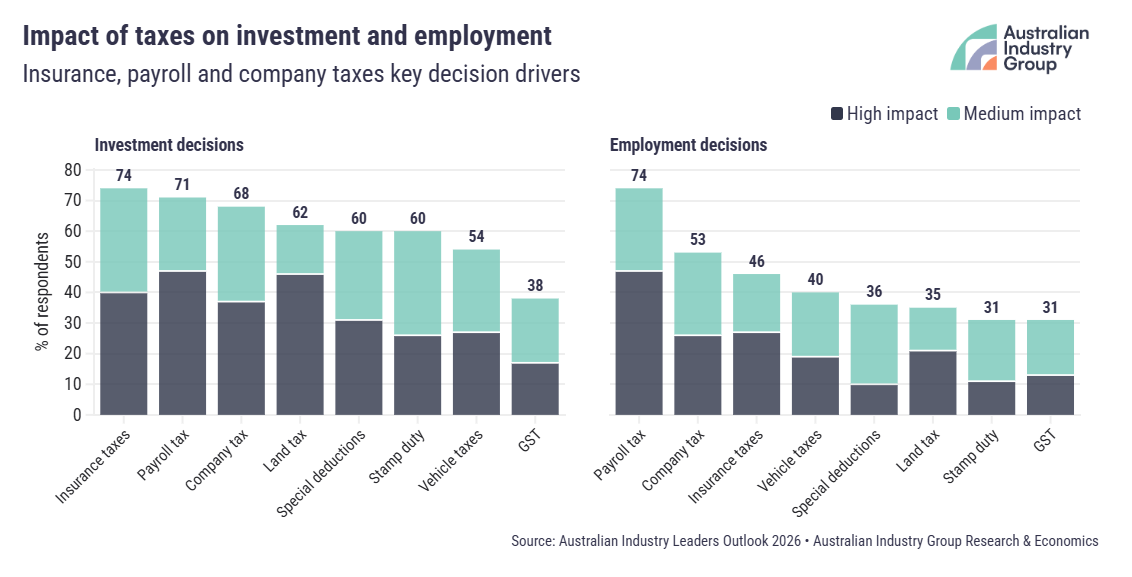

For anyone considering expanding headcount domestically in 2026, the survey included a special panel on tax impacts. Payroll tax was cited by 71% of leaders as having a direct impact on their investment decisions, and by 74% as influencing their employment decisions specifically. That’s not a background concern — it’s the top tax factor shaping whether businesses hire in Australia or not.

Regulatory and compliance sentiment registered -97 net balance — the most negative reading of any factor in the entire survey. Compliance burden is one of the few areas that has not improved for 2026 relative to 2025.

Every domestically hired employee now carries a compliance overhead that goes well beyond salary:

- payroll tax

- superannuation obligations (with Payday Super on the horizon)

- IR obligations under Fair Work reforms

- Right to Disconnect provisions

- insurance levies.

That’s before you factor in recruitment costs and time-to-fill for specialist roles.

55% of leaders nominated reducing payroll tax as their top tax reform priority for 2026, which is ahead of reducing the company tax rate (50%) because payroll tax is especially punishing for job creation and imposes an outsized compliance burden through different state rules.

Until that reform happens (no sign it will happen in 2026), the cost of adding domestic headcount remains structurally elevated. That’s a material input for any CEO’s workforce planning conversation.

Skills Shortages Haven’t Eased Where It Actually Matters

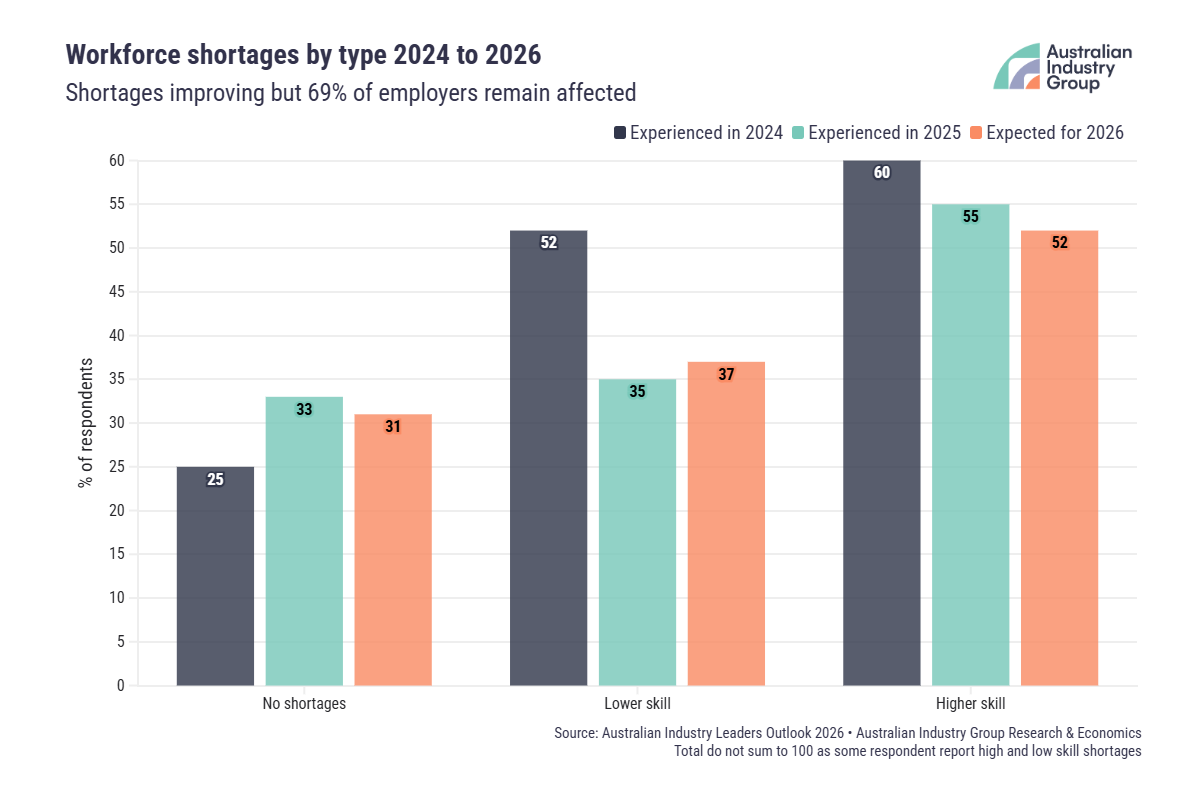

The share of businesses affected by workforce shortages fell from 75% to 67% in 2025. But venture one layer deeper and the picture changes.

Lower-skilled shortage reports fell from 52% to 35% — accounting for almost all of the improvement. Higher-skilled shortages fell only marginally, from 60% to 55%.

The talent pool is looser at the bottom, tighter where it counts.

Construction tells the most pointed version of this story. Constructors report expected shortage rates of 69% for lower-skilled and 78% for higher-skilled occupations in 2026. Every construction-specific occupation is currently listed as in national shortage by Jobs and Skills Australia — the only industry to face universal shortages across all its roles.

It’s not just construction. According to Jobs and Skills Australia, 51% of all persistent occupational shortages nationally are in Technicians and Trades Workers — nearly one in two trade occupations remains in shortage.

Industry leaders do not expect meaningful relief from workforce shortages in 2026. Overall, slightly more businesses expect to be affected by shortages in 2026 (69%) than in 2025 (67%).

Technology Investment Is Growing — But for Different Reasons

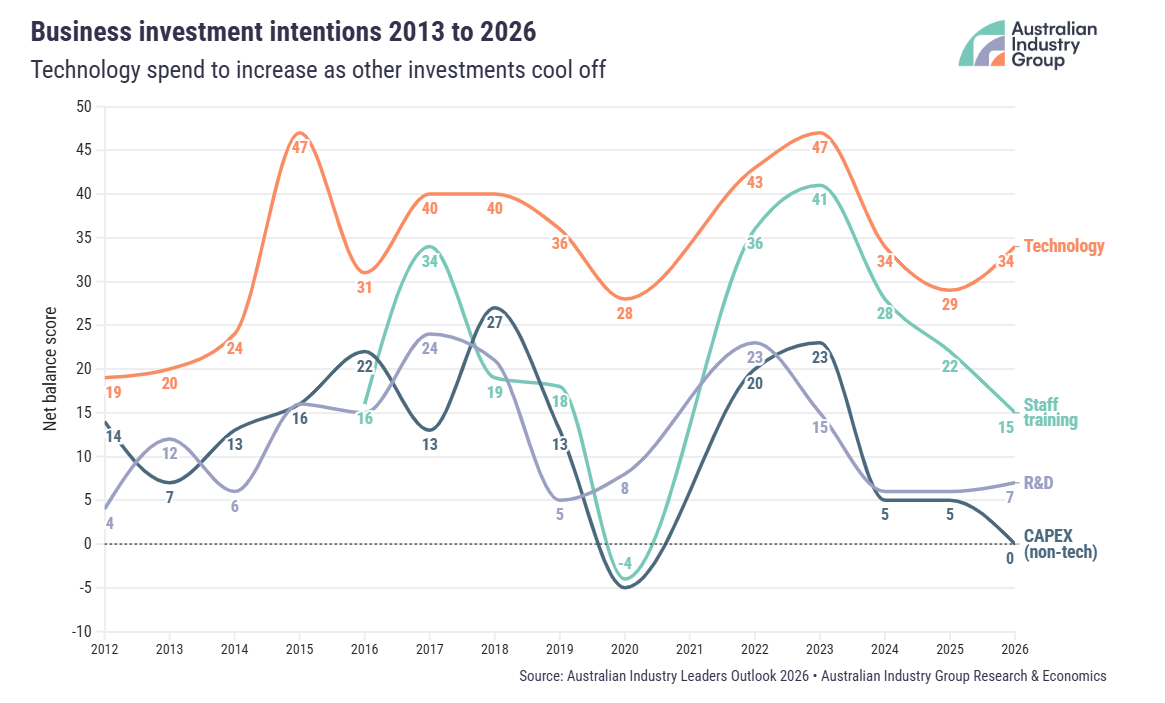

Technology is the only investment category rising in the 2026 survey.

49% of businesses plan to increase technology spending, posting a net balance of +34. Every other major investment category — staff training, capital expenditure, and R&D — is declining or flat.

Business development (59%) and process improvement (50%) are the top-ranked functional priorities for investment in 2026. R&D sits at the bottom at 11%.

This is not technology investment driven by growth ambition. Ai Group’s own researchers describe it as “survival spending” — automation, AI, and process tools being deployed to protect margins rather than build new capability. Technology is being used to do more with a workforce that can’t grow as fast as the work demands.

That creates a specific opportunity for businesses that combine technology investment with a leaner, more flexible workforce structure — including offshore capability for roles that don’t need to sit onshore.

What This Actually Means for Your Workforce Strategy

Here’s our synthesis of what the 2026 data is telling Australian CEOs and staffing firm leaders:

1.

The cost of employing someone in Australia is at a multi-year high — in payroll tax impact, compliance overhead, and wage expectations relative to productivity. That cost is not going down in 2026.

2.

The skilled talent you actually need — in technical, engineering, finance, and professional services roles — is not getting easier to find locally. The headline labour market figures are misleading because the easing is concentrated in low-skill roles.

3.

Your technology investment is protecting margins, not building capacity. If you’re automating to compensate for workforce gaps rather than to expand what your team can do, you’re in a defensive posture.

The businesses in the strongest position heading into 2027 are the ones making structural decisions now — not waiting for the cost environment to improve, and not assuming the domestic talent pool will solve itself.

The smarter move isn’t necessarily hiring more. It’s restructuring how your team is built.

How IMS People Possible Fits Into This Picture

We work with Australian businesses across accounting, engineering support, IT, recruitment operations, administration, and professional services to build dedicated offshore teams that give you access to qualified talent without the domestic compliance overhead.

The model addresses each of the pressure points the Ai Group report identifies directly.

- Rising payroll tax burden? Offshore staff doesn’t sit on your Australian payroll.

- Skills shortage in specialist roles? Our talent pools span qualified finance, engineering, and technology professionals.

- Margin compression from cost increases you can’t pass on? Offshore staffing typically delivers cost reductions of 40–60% compared to equivalent local hires, while you retain full management control.

This isn’t a workaround. It’s a workforce structure that a growing number of Australian businesses are using because the domestic arithmetic, particularly post Fair Work reforms and with payroll tax as it stands, increasingly doesn’t work for scalable operations.

The Bottom Line

The Ai Group’s 2026 Industry Outlook describes an economy recovering, but slowly. Costs are rising faster than revenues. Skilled talent is still constrained where it matters, and a regulatory environment that makes domestic hiring more expensive than at almost any point in the survey’s 13-year history.

None of that is insurmountable. But it does require a deliberate workforce strategy, not a passive one.

If you want to talk through what an offshore staffing structure could look like for your business specifically, IMS People Possible is here for you.